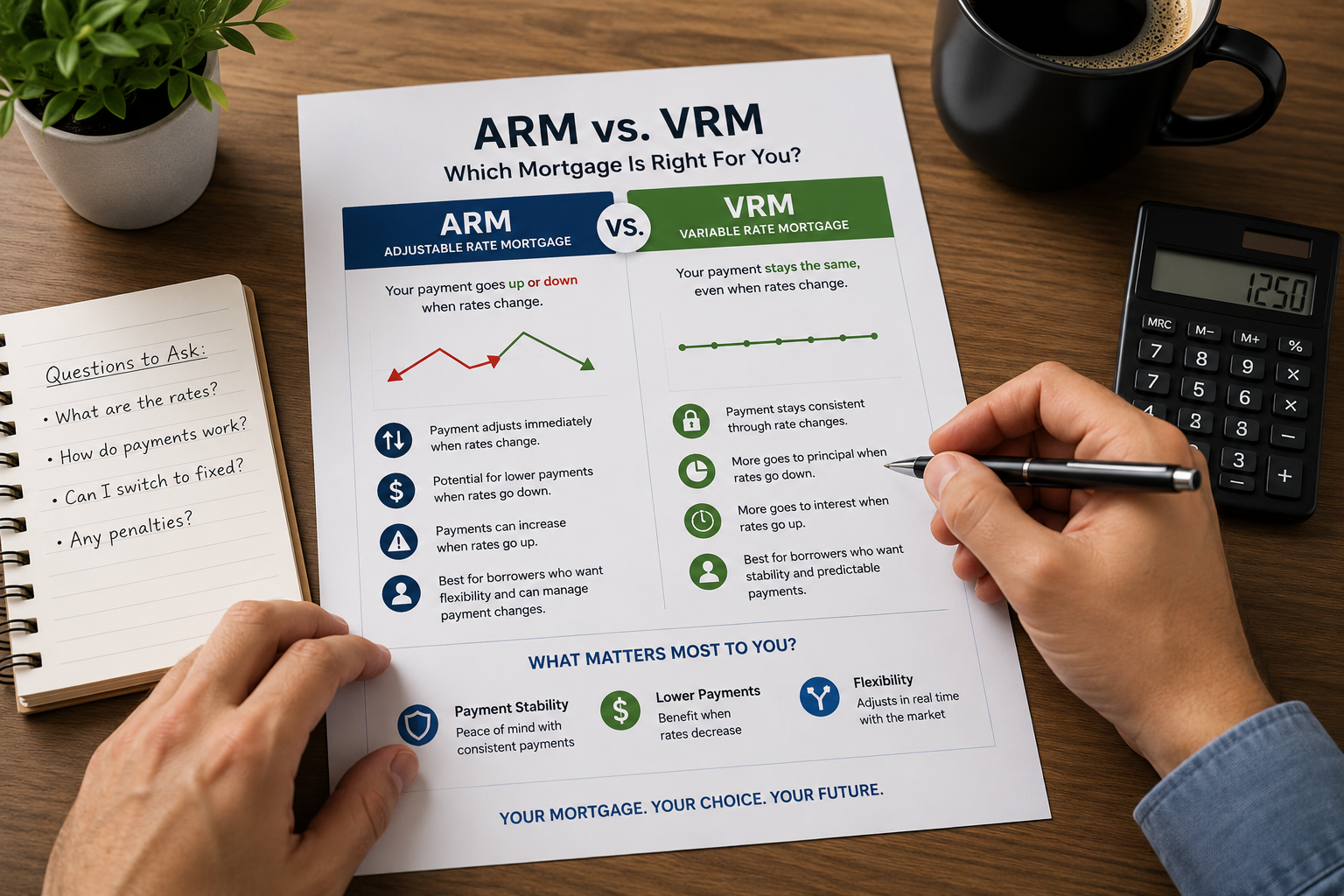

With more Canadians moving toward variable rate mortgages again, you may have also heard about something called an Adjustable Rate Mortgage (ARM). At first glance, they seem similar. Both move with prime rate changes. But the way they behave can feel very different once rates start moving.

Here's the simple breakdown.

Variable Rate Mortgage (VRM)

Think of a VRM like cruise control.

Your interest rate changes when prime changes, but your payment usually stays the same. What changes behind the scenes is how much goes toward interest versus principal.

When rates go up:

- More of your payment goes toward interest

- Less goes toward paying down your mortgage

- In extreme cases, it can lead to negative amortization

When rates go down:

- More of your payment goes toward principal

- You pay off your mortgage faster without changing your payment

A VRM can work well for borrowers who prefer payment stability and don't want monthly payments constantly changing.

Adjustable Rate Mortgage (ARM)

An ARM reacts immediately to rate changes.

If prime rate goes up, your payment goes up. If prime rate goes down, your payment goes down automatically.

This option is popular for borrowers who:

- Are comfortable with payment fluctuations

- Want to benefit immediately from falling interest rates

- Prefer their mortgage to adjust in real time

In today's market, some ARM products may offer better flexibility because your payment naturally drops as rates decline — instead of waiting for renewal.

Which Mortgage Is Better?

There's no one-size-fits-all answer.

A VRM may be better if:

- You want predictable payments

- You prefer budgeting consistency

- You can handle slower principal paydown during higher-rate periods

An ARM may be better if:

- You believe rates will continue falling

- You want lower payments automatically when rates drop

- You're comfortable with short-term payment changes

Can You Switch to a Fixed Rate Later?

Yes.

Most banks and monoline lenders in Canada allow borrowers to convert from a variable or adjustable mortgage into a fixed-rate mortgage during the term.

This can be useful if:

- Rates start rising quickly

- You want long-term payment stability

- You simply want peace of mind

Many lenders allow this conversion without a traditional mortgage break penalty because you're staying with the same lender and simply changing products. However, the new fixed rate offered will usually be based on the lender's current rates and terms.

Final Thoughts

The "best" mortgage isn't always the lowest rate. It's the mortgage that matches your comfort level, cash flow, and long-term plans.

Whether you choose an ARM or VRM, understanding how each product reacts to changing interest rates can help you make a smarter financial decision in today's market.

Your Mortgage. Made Better.